Are you on track for retirement? Statistically speaking, not likely. Today, most Americans have less than $1,000 saved for retirement and 50% have nothing saved (Economic Policy Institute, 2016). The research shows there are several reasons we aren’t saving enough — overwhelming debt, stagnant salaries, family expenses, lifestyle creep, etc.. That aside, many of us simply are not educated on the importance of saving, especially for a goal that may seem so far away.

Regardless of where you are, remember that it is never too early or too late to start saving. As with many things, I often find that the most difficult barrier is getting started. We tell ourselves how important it is to eat well, exercise regularly, plan for the future, etc… but our emotions often get the better part of us. My motivation to get to the gym, for example, is often low. But once I get in the car and start heading in that direction, I’ve overcome the most difficult part. And once I complete a workout — I am thanking myself for making that initial decision to just go.

I became a financial advisor for the same reason I became a teacher — to help transform communities.

I became a financial advisor in part because I saw my parents struggle with their personal finances. It is not that my parents did not earn a living wage, it is that we consistently lived beyond our means.

As your financial advisor, I believe it is my job to stand beside you throughout life’s challenges and successes. It is my job to help you develop a plan that is based on your personal goals and objectives. It is my job to be your accountability partner on your path to pursuing those goals. But I cannot just tell you that and expect your actions to change. It starts with your own mindset around money. What do you value? How important are your goals to you?

HOW MUCH SHOULD I BE SAVING IN A RETIREMENT ACCOUNT?

As always, the answer often depends on your individual story and what you envision for YOUR retirement. That said, here are some things to consider.

-

Start early OR start today. If you’re just starting out your career, now is the time to begin building the financial habits that will allow you to take advantage of time — you have many working years ahead. When I started my career as a teacher, a mentor of mine shared the importance of contributing to a retirement account — 10 years later, I am increasingly appreciative of that advice. For those of you playing a bit of catch-up, start today — your future self with thank you. For those age 50 or older, you are eligible to make “catch-up contributions” as well.

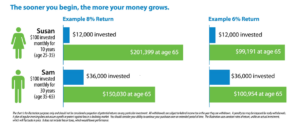

If you’re not yet adulting, let me help. Maybe you’re a working professional but still living with your parents. If your financial commitments are limited to yourself — no spouse, mortgage, children, etc. — right now may be the perfect time to front-load your savings. Your life (and finances) could look very different in 10 years. Below is an illustration that highlights the importance of starting early and the power of compounding — you can also check out a video here.

-

Set a goal to save 15% of your income. It’s not about how you start, but how you finish — first, you need to start. Maybe today you start with 5% and increase each year. It is the contribution rate that is going to drive your retirement success. If you’re not saving enough, the best investment is not going to help create the retirement that you envision. If you’re able to contribute a percent (%) rather than a flat dollar amount, do so. As you earn more, your contributions will automatically increase.

Example: If you earn a $55,000 salary and get paid 26x per year ($55,000/26), your pay before taxes is about $2,115. Therefore, a 5% contribution = $105, 10% = $211, 15% = $317.

The number-one factor in determining how much you’ll have at retirement is the amount you save throughout your career.

- Take advantage of your company match. If your employer offers to match your contributions, you should be contributing at least to the amount they will match. This is free money! If they match up to 5%, you should be contributing at least 5%. Otherwise, you risk leaving money on the table that would have been given to you otherwise.

-

Make it automatic. We are emotional human beings — if left to our own devices, we often choose to save last, if we have enough money left over each month. “Pay yourself first” is a mindset that puts YOU first. Take the emotion out of the decision and put your retirement saving at the top of what you have to pay each month. If your employer offers an option to increase your contribution automatically each year, take advantage of it! Otherwise, set a reminder or work with your advisor to serve as your accountability partner.

But I will have a pension. Should I still save 15%?

If you’re an educator or a government employee, you may be eligible for a pension. I am always in favor of taking charge of the things that I can control. I earned my Masters in Education from Harvard and I thought I would serve as a counselor (or school administrator) for the duration of my career. My life had different plans — had I relied on my TRS pension and not saved in a retirement account, I’d be kicking myself. Although I will be eligible for a pension from TRS one day, it will be minimal compared to a career educator of 35+ years. Life happens every day — I have clients who thought they would be able to work until age 65 but have been forced into retirement due to health reasons. Change is the only constant.

That said, if you are well into your career and expect to be eligible for a modest pension based on your average salary and years of service, maybe your needs in retirement will not be as much. I’d prefer to have to scale down my contributions rather than scale up.

My values drive my decisions

What is important to you? That is for you to decide and for us to work on together. Let’s get you to your best financial self. As with many things are that are new or different, the hardest part is often getting started. It’s not about how you start, but how you finish — first, you need to start.

LET’S MAKE A PLAN!

I know that you’re busy and it’s not always easy to make sense of your personal finances. There is no substitute for having a plan. Whether you’re just starting out or interested in learning more, I am happy to be a resource along the way.

Schedule a Meeting: In person or virtual

Jesse is a graduate of the University of Notre Dame and earned his Master’s in Education from Harvard. In his education career, he served as a teacher, counselor and Director of Alumni for YES Prep Public Schools. He is a member of the Teacher Retirement System of Texas (TRS) and takes pride in helping fellow educators better understand their pension and plan for their future. Learn more about Jesse.