At Dearborn & Creggs, we have been working with Texas educators and city and county employees for 30 years. As a result, we have made it our business to support our clients with their state pensions. I will use the Teacher Retirement System (TRS) pension as an example in this blog post, however, the ideas here could be applied to other pension plans as well.

As you may have guessed, the answer to the question above is a resounding YES! But there’s more. Knowing the basics about how your pension works could help you know how much you should be saving and when you should retire. Pensions are rare these days and can be a powerful piece of your retirement planning. As a TRS member, you may have what is called a defined benefit plan or annuity. This means that you may be eligible for a monthly payment starting when you retire. Your monthly pension is for life!

That said, your pension shouldn’t be viewed as your only source of income in retirement. Depending on what you envision for your retirement, it is likely important that you also have personal savings in the form of a 403(b), 457, IRA, etc.. Your pension is not adjusted for inflation — so if your monthly pension is $3,000 in 2020 — it will also be $3,000 in 2050. You will not want to return to work in your retirement years out of necessity! If you do work, it should be because you want to. THAT is financial freedom.

The power of compounding is the single most important reason to start investing now.

If you have many years ahead before retirement, plan for the unexpected. Although you’re in education today, you may decide to work for a non-profit that doesn’t contribute to TRS in the future or change careers altogether. Additionally, TRS is a state pension program and although it is an important benefit to many retirees, it may not look exactly the same in 20, 30 or 40 years. It is not in your control. Start contributing today to an account that is completely yours and your future self will thank you. The longer you invest, the longer your money has to grow and compound. (see Am I saving enough for retirement?)

If you’re near retirement, it is not too late. Start by calculating your expected pension and take it for a test drive (seeTake your retirement for a test drive). For example, if your expected monthly pension will be $3,000, base your monthly budget on that starting today. If you see that you will need more in retirement, you may need to make adjustments to the number of years you have left to work or your savings rate.

YOUR TRS PENSION IS JUST ONE PIECE OF THE PIE

Let’s throw some numbers in to make this a bit more real. Understandably, your situation will vary but hopefully you can plug your own numbers in to help with your decision. I’m also happy to help.

Below is the formula TRS uses to calculate your pension. It is the same formula for all TRS members and you can plug in your expected numbers to get an idea for yourself. (Note: When you’re eligible for normal age retirement will depend on what Tier you’re in. This can be viewed on your TRS statement. More on that in a separate post or in a conversation with me.)

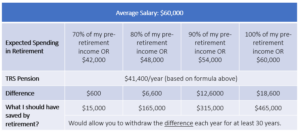

Let’s assume Mr. Teacher would like to retire at age 60 but would like to see if that would make sense for him. Here are the variables I am using for this hypothetical example:

-

Average Highest Salary: $60,000

-

Years of Service in a TRS position: 30 years

Plug Mr. Teacher’s numbers in: $60,000 x 2.3% x 30 = $41,400/year or $3,450/month.

Regardless of where you are in your career, this is great information to have, because it gives you a starting point. Will that be enough for you? That depends on you and your expenses, mostly. The current consensus is that you will need between 70-90% of your pre-retirement income in retirement. Although it may be easy to assume that you will spend less in retirement, about half of retirees end up spending more, according to the Employee Benefit Research Institute (EBRI).

YOU WILL NEED ADDITIONAL SAVINGS — HOW MUCH, DEPENDS

As you know, it is difficult to predict what our future expenses will be. We will take a look at some hypothetical examples below. You know yourself best. If you’d like to err on the side of caution, you can look at the 90% or more columns. I don’t think anyone would complain about having saved too much! If you’re closer to retirement now, you may be able to look at your current expenses as a place to start.

These estimates are based on The 4% Rule, a rule of thumb used to determine how much a retiree could withdraw from a retirement account each year for 30 years without running out of money. Try it out for yourself! https://www.dearborncreggs.com/resource-center/retirement/a-look-at-systematic-withdrawals

In the case of Mr. Teacher, if he plans to retire at age 60 with 80% of his pre-retirement income, he would need to have saved about $165,000 in his retirement account over his career. If he has not saved that amount, he may need to look at some alternatives to reach his goal.

OTHER WAYS TO MEET YOUR GOAL

-

Increase your salary (and not your expenses): Remember, your TRS pension is based on your highest 3 or 5 years of salary. As we saw above, 69% of $60,000 is $41,400 but 69% of $80,000 or $100,000 would make a big difference for your retirement income as well.

-

Work longer: Every year more that you work, your pension eligibility goes up by 2.3%. In the example, I used 30 years, which when multiplied by 2.3% is 69%. 35 years x 2.3% is 80.5%.

-

Save more: Maybe you’re playing catch up from not saving before or maybe you don’t want to work 35 years before you can retire. Those are both appropriate reasons to increase your savings rate so that you have more choices as you get closer to retirement.

WHAT IF I DON’T HAVE A PENSION?

If you do not have a pension, it is likely that you are paying into Social Security and will have a benefit available to you once you retire. It is not advisable to depend on it as your only, or even your primary, source of income in retirement. According to Social Security, if you have average earnings, your SS benefit will replace only about 40% and even less if you’re a high-income earner. Develop a plan to save a portion of your income and work to increase your savings over time.

LET’S MAKE A PLAN!

I know that you’re busy and it’s not always easy to make sense of your personal finances. There is no substitute for having a plan. Whether you’re just starting out or interested in learning more, I am happy to be a resource along the way.

Schedule a Meeting: In person or virtual

Jesse is a graduate of the University of Notre Dame and earned his Master’s in Education from Harvard. In his education career, he served as a teacher, counselor and Director of Alumni for YES Prep Public Schools. He is a member of the Teacher Retirement System of Texas (TRS) and takes pride in helping fellow educators better understand their pension and plan for their future. Learn more about Jesse.